24.07.2024 / New LCV market forecast for 2024-2025

The new light commercial vehicle (LCV)[*] market forecast is based on three scenarios: baseline, optimistic and pessimistic.

According to all three forecast scenarios, the following factors have a negative impact on the Russian automotive market.

1. Sanctions (EU, USA and other countries). After February 24, 2022, economic sanctions were imposed against the Russian Federation, which also affected the automotive market. There is a ban on the export of LCV, automotive components for manufacturers, spare parts, technologies and equipment to the Russian Federation. Nevertheless, the Russian automotive market has adapted to the new conditions: most of LCV supplied from countries that have announced sanctions against the Russian Federation have been replaced with Russian ones. In addition, the import of Chinese LCV is expanding, a small amount of LCV of brands that have left the Russian market is supplied under alternative import. Based on global political trends, we assume that sanctions against the Russian Federation will remain in 2024-2025.

2. High loan and leasing interest rates. On December 18, 2023, the Central Bank of the Russian Federation raised the key rate to 16%. This rate is valid in January-July 2024. With the growth of the key rate, the loan and leasing interest rates increased, which made these financial instruments less affordable. The negative impact of high leasing and loan interest rates will continue in the second half of 2024 and in 2025. Leasing and loan interest rates will depend on the key rate of the Central Bank of the Russian Federation, which may be increased in the second half of 2024 or in 2025.

3. Tightening the auto lending conditions for individuals with a high debt burden. On July 1, 2024, the Central Bank of the Russian Federation established surcharges to the risk ratios for auto loans with a debt burden index (DBI) exceeding 50%. Their value varies from 1.7 for DBI of 50-60% to 2 for DBI of over 80%. It will be more difficult for consumers with a high debt burden to get a loan. At the same time, banks may continue to lend to some borrowers with high DBI, increasing loan terms for them and thereby reducing the debt burden.

Changes in the lending terms that became valid on July 1, 2024 will have a less significant negative impact on new LCV sales, since the bulk of vehicles is purchased not by individuals, but by legal entities.

4. The growth of recycling tax and stricter conditions for certification of imported vehicles. In August 2023, the recycling tax rates for LCV increased. Given that Russian manufacturers that have signed the SPIC are compensated for the recycling tax costs in the form of industrial subsidies, its increase primarily has a negative impact on prices for Chinese and other imported vehicles. Also, beginning April 1, 2024, taxes and fees that were not paid due to underestimation of the customs value of vehicles imported into the Russian Federation from the EAEU countries are taken into account as part of the recycling tax. The recycling tax for LCV is expected to increase on October 1, 2024. In 2025, further indexation of recycling tax coefficients is expected.

Since October 1, 2023, certification of vehicles of those brands that have not stopped official deliveries to Russia and are not included in the list of brands allowed for parallel import has been carried out under the Technical regulations "On the safety of wheeled vehicles". Vehicle Type Approval is issued for vehicles of these brands, previously it was possible to issue Conclusion on the Assessment of a Single Vehicle under a simplified procedure. Legal entities are required to install the ERA-GLONASS system when importing vehicles. These requirements will remain in the second half of 2024 and 2025.

The growth of recycling tax and stricter conditions for certification of imported vehicles results in increase in LCV prices, which has a negative impact on the market.

5. Release of pent-up demand. The pent-up demand of carriers and companies from other fields of activity in new LCV was partially satisfied in 2023, and they will not intensively renew and expand their fleets in 2024-2025.

6. Tax reform in 2025. In 2025, tax reform will be carried out in the Russian Federation and the tax burden on companies and individual entrepreneurs will increase, which will lead to a further increase in prices for vehicles, spare parts, service, etc. Against the background of the growing tax burden, high auto loan rates and rising prices, private consumers will postpone their decision to purchase vehicles. Corporate clients will have reduced financial capacity to renew their LCV fleets.

Nevertheless, there are factors that make it possible to smooth out the negative trends in the new LCV market in 2024-2025.

1. State support measures for the market of LCV running on traditional fuel and electric LCV.

In 2024, state support measures are in place for the LCV market. First of all, these are preferential auto loan programs (cars and LCV, including electric cars), for which 17.3 billion rubles were allocated in 2024, and 23.1 billion rubles will be allocated in 2025.

In 2024, preferential leasing programs cover not all LCV, but only minibuses and LCV equipped with electric motors. 9 billion rubles were allocated for these programs in 2024 (tractor units, unmanned trucks, buses, minibuses, and electric cars including LCV equipped with electric motors). In 2025, the preferential leasing programs will continue with a budget of 11 billion rubles (for all types of vehicles that will fall under the program).

In 2024, LCV will be subject to procurement under the program for converting vehicles to natural gas fuel under Decree of the Government of the Russian Federation No. 669 dated 05/13/2020, but the expected volumes of such procurement have not been officially published. LCV procurement is also planned as part of the School Bus program. It is planned to allocate 10 billion rubles for the purchase of school buses in 2024. With this money, it is planned to purchase at least 3,000 school buses (minibuses and buses of various classes).

As for LCV equipped with electric motors, reduced recycling tax rates, the possibility of free travel on toll roads and a number of regional benefits are valid in 2024, in addition to preferential auto loans and leasing. Nevertheless, electric LCV sales in the Russian market in 2024-2025 are expected to remain relatively low compared to those of traditional vehicles.

2. Development of e-commerce and e-trading. In the first quarter of 2024, the volume of e-trading increased by 39% on the similar period last year and amounted to 1.9 trillion rubles[†]. . E-commerce is also projected to grow by the end of 2024. In 2024-2025, the development of e-commerce and the growing demand for small delivery vehicles from marketplaces and transport companies serving them will become an incentive for the development of the new LCV market.

3. Return of LADA Largus vehicles to the LCV market. On June 2024, LADA Largus vehicles returned to the LCV market. According to official AvtoVAZ data, their production began on May 15, 2024. In 2024, sales of LADA Largus light commercial vehicles will not be very high, since in the first half of the year these vehicles were practically not available on the market. In 2025, sales of LADA Largus vehicles can be expected to grow on 2024.

4. Standard LCV replacement cycles. In 2024 and 2025, old, worn-out and broken down vehicles will be retired from the fleets of private and corporate vehicle owners and replaced with new ones.

5. Negative consumer expectations. In anticipation of rising prices for LCV, a possible increase in loan and leasing interest rates, and a possible depreciation of the ruble, some corporate and private consumers will purchase LCV at the current time so as not to overpay for them in the future.

This behavior of some consumers will remain in the second half of 2024 and in 2025 and will continue until the situation with prices, loan and leasing interest rates, and inflation in the automotive market stabilizes.

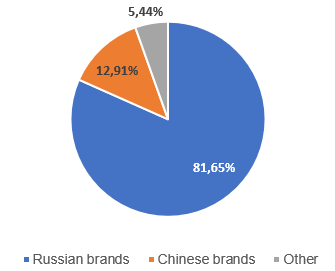

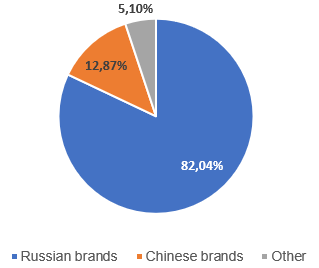

According to all forecast scenarios, Russian and Chinese brands will dominate in the Russian LCV market in 2024-2025. New vehicles imported under parallel import and those of foreign brands manufactured on the territory of the People's Republic of China and "friendly" countries to the Russian Federation will also be sold.

The baseline forecast scenario assumes the following:

2024

- the key rate of the Central Bank of the Russian Federation may be increased by 1-2 percentage points in the second half of 2024, which will lead to a further increase in the cost of loans and leasing,

- additional financing for state preferential auto loan and leasing programs will not be allocated in the second half of 2024,

- the macroeconomic situation in Russia will remain difficult. GDP in 2024 may grow by 2.5% on 2023, inflation will be 6.1%.

2025

- the key rate of the Central Bank of the Russian Federation in 2025 will remain at the level of the second quarter of 2024, lending and leasing of cars will remain expensive,

- the macroeconomic situation in Russia will remain difficult. GDP in 2025 may grow by 1.6% on 2024, inflation will be 5.2%.

The optimistic forecast scenario assumes the following:

2024

- the key rate of the Central Bank of the Russian Federation in the second half of 2024 will remain at the level of 16% and there will be no significant increase in the cost of lending and leasing,

- additional financing may be allocated for preferential auto loan and leasing programs in the second half of 2024,

- the macroeconomic situation in Russia will remain difficult. GDP in 2024 may grow by 2.7% on 2023, inflation will be 5.1%.

2025

- the key rate of the Central Bank of the Russian Federation may decrease by several percentage points in 2025, lending and leasing of cars will become more affordable,

- the macroeconomic situation in Russia will remain difficult. GDP in 2025 may grow by 1.8% on 2024, inflation will be 4.2%.

The pessimistic forecast scenario assumes the following:

2024

- the key rate of the Central Bank of the Russian Federation may be increased by more than 2 percentage points in the second half of 2024, which will lead to a further increase in the cost of loans and leasing of vehicles,

- additional financing for state preferential auto loan and leasing programs will not be allocated in the second half of 2024,

- the macroeconomic situation in Russia will remain difficult. GDP in 2024 may grow by 2.0% on 2023, inflation will be 7.1%.

2025

- the key rate of the Central Bank of the Russian Federation will continue to grow in 2025, therefore, interest rates on loans and leasing will increase,

- the macroeconomic situation in Russia will remain difficult. GDP in 2025 may grow by 1.4% on 2024, inflation will be 6.2%.

New LCV sales forecast for 2024-2025

| Sales forecast, scenario |

LCV sales forecast in 2024, thousand units |

Growth/loss, 2024/2023, % |

LCV sales forecast in 2025, thousand units |

Growth/loss, 2025/2024, % |

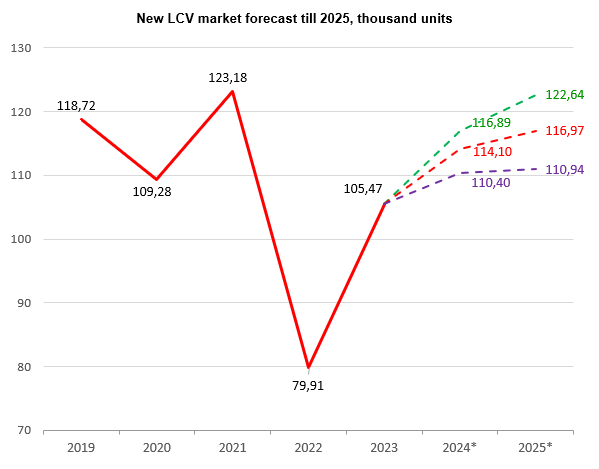

| Optimistic scenario | 116.89 | 10.83 | 122.64 | 4.92 |

| Baseline scenario | 114.10 | 8.19 | 116.97 | 2.52 |

| Pessimistic scenario | 110.40 | 4.68 | 110.94 | 0.48 |

Source: NAPI (National Industrial Information Agency)

New LCV market forecast till 2025, thousand units

* forecast

Source: NAPI (National Industrial Information Agency)

New LCV market composition forecast in 2024, baseline scenario

Source: NAPI (National Industrial Information Agency)

New LCV market composition forecast in 2025, baseline scenario

Source: NAPI (National Industrial Information Agency)

[*] Vehicles with GVW of up to 6 tons inclusive, including pickups

[†] Data by Association of Internet Trade Companies (AKIT)

Press-release archive

Information

Market analysis

Spare parts market analysis

Spare parts market analysis

Automotive statistics

Automotive statistics

Automotive leasing

Automotive leasing

IT-solutions for automotive market analysis

IT-solutions for automotive market analysis

Taxi population in Russia

Taxi population in Russia

Dealers

Dealers

Vehicle ownership period

Vehicle ownership period

Corporate vehicle market

Corporate vehicle market

Total cost of ownership

Total cost of ownership

Special purpose vehicle

Special purpose vehicle

Legal factors affecting automotive market formation

Legal factors affecting automotive market formation

Vehicle prices

Vehicle prices

Residual value of cars and special purpose vehicles

Residual value of cars and special purpose vehicles

Forecasts

Forecasts